During July, I continued withdrawing funds from Mintos and increasing my Income marketplace portfolio. The yields offered to investors on Mintos have reduced gradually in the past year or two, probably driven by many of the LO´s being able to raise cheaper funding outside of P2P marketplaces. The decreasing yields are not only limited to Mintos, but can be also observed on other marketplaces (e.g. Peerberry). It seems that at the time of writing for >12 month EUR denominated loans, investors can expect to currently earn about 10% p.a. This trend is something that P2P investors should get used to, as decreasing yields are likely to continue, but even lower yields, can still be attractive, provided that there is additional protection for invested capital.

My auto-invest strategies on Income marketplace have been mostly set to pick loans with a 12% p.a. yield, so my strategy of remaining over 10% p.a. in P2P investments is holding. So far I’ve earned 11.85% on Income marketplace vs 10.67% p.a. on Mintos.

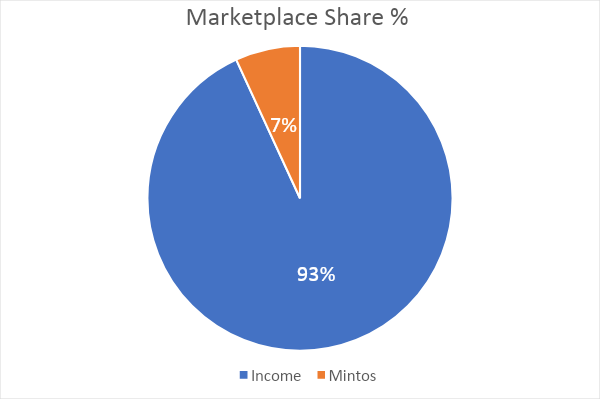

Portfolio split by marketplace

I’m currently invested in two marketplaces. My P2P portfolio increased from the previous month (€56,210) to €57,697, and is divided between Mintos 7% (vs previous month 15%) and Income marketplace (93%). I don’t see myself returning to Mintos, but I may try other crowdfunding sites such as Estateguru in the coming months.

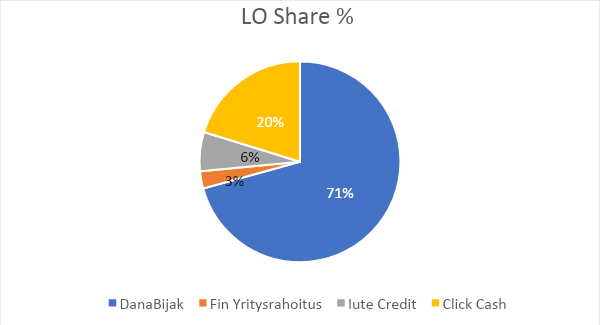

Portfolio split by LO

Both Iute Credit and ESTO loans have been amortizing as expected, and are starting to represent only a small part of my portfolio. I’ve removed ESTO this month from the split, as I only have less than 1% of my portfolio now there.

Danabijak’s share (71% vs 67% last month) of my portfolio increased again. Danabijak introduced installment loans to the listings, which have slightly longer maturities, so I decided to invest in those also. ClickCash grew from 16% to 20% in my portfolio and FIN-Y increased to 3% from 2% in previous months.

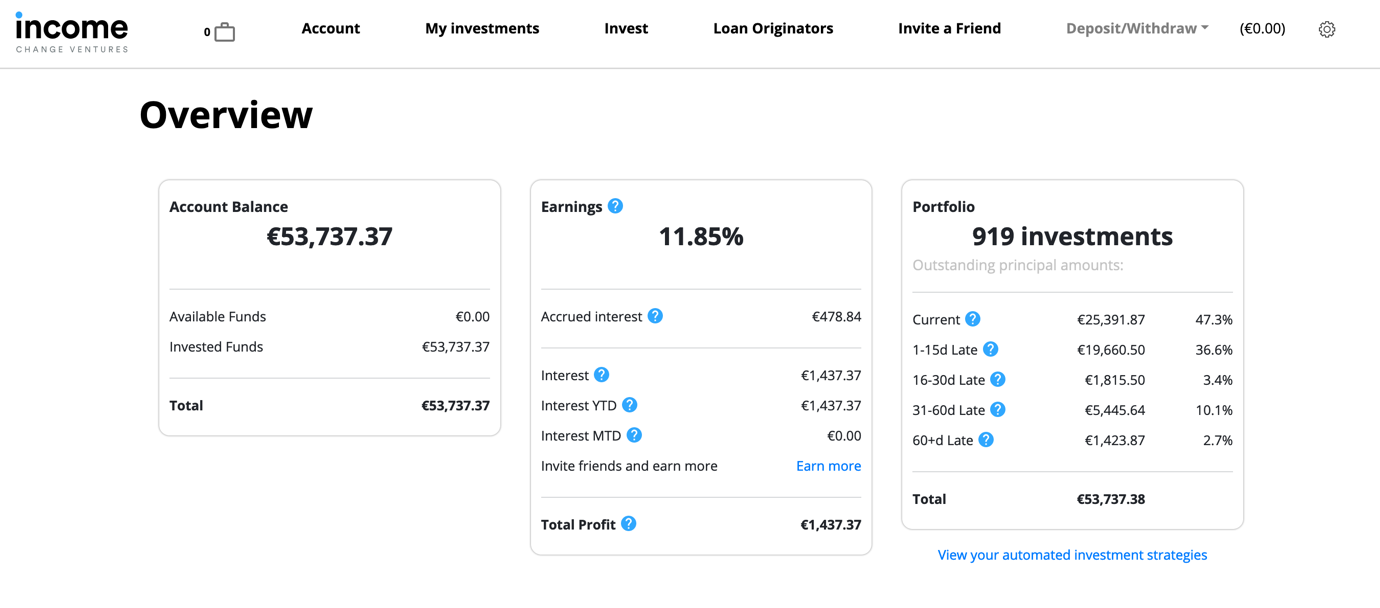

Income Account overview

I’ve been investing on Income marketplace since the end of January and have gradually increased the size of my investments. I’ve since earned 11.85% on my investments p.a., which equals €1,437.37. I have also accrued €478.84 of interest on my investments, which will move to the “interest” and “total profit” line when the next payments from the LOs come.

Income marketplace does not have pending payments, so the 1-15 day late “bucket” I normally don’t pay too much attention to, as it is normal for borrowers to pay their loans a few days late. Also the clearing days of LO payments and buyback guarantees are Tuesdays and Fridays, so this inflates the 1-15DPD bucket and 60+d (Buyback) late buckets. A fix to more clearly visualize the portfolio split is on the way from Income.

My portfolio split of 47.3% in current and 36.6% in 1-15 day late can therefore be considered normal and no cause for alarm. The same goes for the 60+d late, which will be bought back by the LO on the next clearing day.

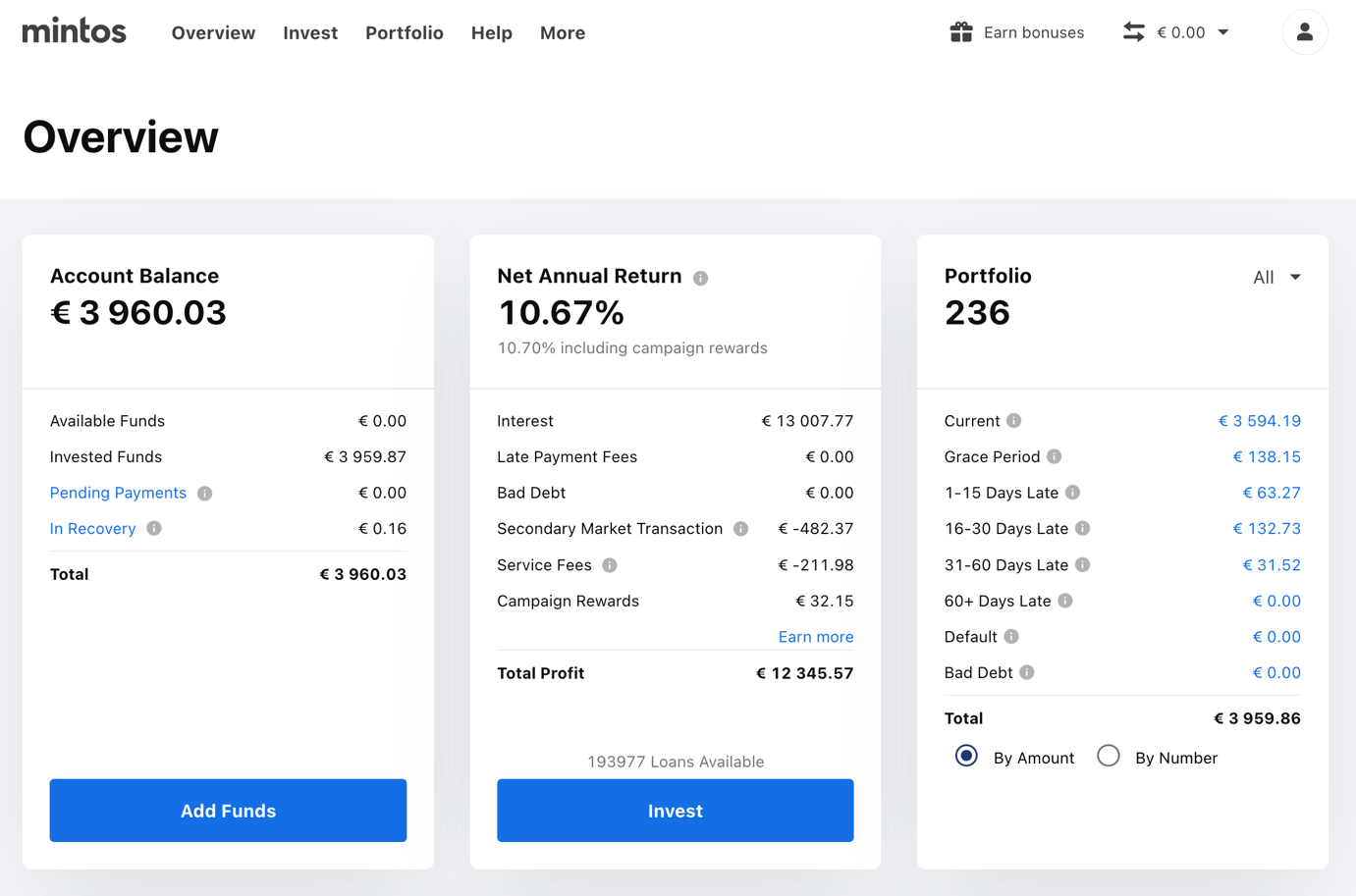

Mintos Account overview

I started investing on Mintos in 2019 and quickly grew my portfolio to over €100,000. I´ve since earned 10.66% on my investments p.a., which equals €12,245.58.

Conclusion

My portfolio in July did not provide too many surprises, and kept giving me the expected yield. On Mintos the two loan originators I’ve been investing in (Iute Credit and ESTO) seem to perform better in loans than pre-covid, which I find interesting. Anothertrend I’ve been observing for a longer time already is loan originators setting up their own related party loan platforms. Examples include Afranga (Stikcredit), Lendermarket (Creditstar), Esketit (Cream Finance), and possibly also Iute Credit has its own platform planned, judging from the ads they are running on Facebook. It seems that for an investor to have a diversified portfolio, they will in the future have to have accounts on many different platforms, which is a bit of a hassle. However the main thing to keep in mind is that more important than diversification is capital protection, and investors should only invest on platforms where they can see their interests are sufficiently protected.